Streamline Your Period-End Review Closing Process with Our Procedure Template Word Product

Are you tired of the stress and confusion that comes with the period-end review closing process? Look no further than our Period-End Review Closing Process Procedure Template Word product.

This comprehensive template is designed to help you streamline your period-end review closing process, ensuring that everything is completed accurately and efficiently. With step-by-step instructions and customizable sections, you can tailor the template to fit the unique needs of your business.

Our Period-End Review Closing Process Procedure Template Word product includes sections for reviewing financial statements, reconciling accounts, and preparing journal entries. It also includes a checklist to ensure that all necessary tasks are completed before closing the period.

By using our template, you can save time and reduce the risk of errors during the period-end review closing process. Plus, you can rest easy knowing that your financial statements are accurate and up-to-date.

Our Period-End Review Closing Process Procedure Template Word product is easy to use and can be downloaded instantly. It is compatible with Microsoft Word, making it easy to customize and edit as needed.

Don’t let the period-end review closing process cause you stress and headaches. Streamline your procedures with our Period-End Review Closing Process Procedure Template Word product today.

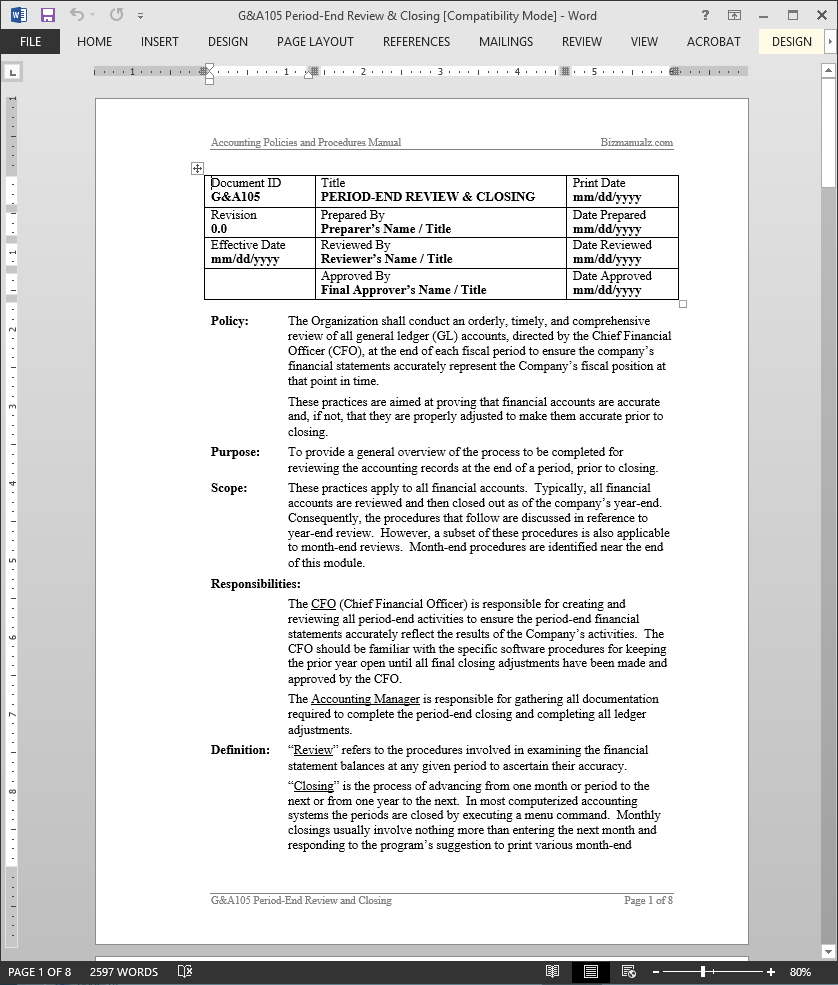

Period-End Review Closing Procedure

The Period-End Review Closing Procedure provides a general overview of the process to be completed for reviewing the accounting records at year-end or any particular month-end prior to closing.

The practices mentioned in the Period-End Review Closing Procedure apply to all accounts. A subset of this period review procedure is also applicable to month-end reviews, although, typically, all financial accounts are reviewed and then closed out as of the company’s year-end. (8 pages, 2559 words)

Period-End Review Closing Definitions:

Review – the procedures involved in examining the financial statement balances at any given period to ascertain their accuracy.

Closing – the process of advancing from one month or period to the next or from one year to the next. In most computerized accounting systems the periods are closed by executing a menu command. Monthly closings usually involve nothing more than entering the next month and responding to the program’s suggestion to print various month-end reports. Even after moving to the next month, many accounting systems allow the user to return to previous months to enter or edit transactions.

Period-End Review Closing Responsibilities:

The CFO (Chief Financial Officer) is responsible for creating and reviewing all period-end activities to ensure the period-end financial statements accurately reflect the results of the company’s activities. The CFO should be familiar with the specific software procedures for keeping the prior year open until all final closing adjustments have been made and approved by the CFO.

The Accounting Manager is responsible for gathering all documentation required to complete the period-end closing and completing all ledger adjustments.

Accounting Month End Close Checklist Activities

Accounting Month End Close Checklist Activities

- Period Closing Preparations

- Balance Sheet: Assets Review

- Balance Sheet: Liabilities and Stockholders’ Equity Review

- Income Statement: Revenue Review

- Income Statement Expense Review

- Financial Ratio Analysis

Accounting Period-End Review & Accounting Month End Close

An orderly, timely and comprehensive review of all general ledger accounts should be performed or directed by the CFO on a regular basis to ensure an accurate representation of the company’s financial statements.

Typically, all financial accounts are reviewed and then closed out as of the company’s year-end. These practices are aimed at ensuring that the financial accounts are accurate, and if not, are properly adjusted to make them accurate, prior to closing.

What is an Accounting Review?

An Accounting “Review” refers to the procedures involved in examining the financial statement balances at any given period to ascertain their accuracy. Accounting is a double-entry system. Thus, each business transaction has two equal sides. Your accounting review ensures everything is in balance. Because of this interdependence, the accuracy of the income statement is dependent upon the accuracy of the balance sheet. Although, the impact of the actual transaction differs if your are using cash accounting or accrual accounting.

CASH ACCOUNTING REVIEW

Cash accounting is based on your cash transactions. Items are entered (dated) onto your financial statements when the cash transaction occurs.

For example, If you receive a bill for an expense, the entry is dated when the bill is paid. Paying an expense decreases cash on the balance sheet and increases an expense on the income statement. Getting paid for a service or sale increases cash on the balance sheet and increases revenue on the income statement.

ACCRUAL ACCOUNTING REVIEW

Accrual accounting is based on expectations of a future event. Sales are entered as they occur and a second entry is made in receivables, if we are waiting for the cash, or in a cash account if the sale was accompanied with a payment.

For example, (using accrual accounting) when a bill is received, an expense entry is made in the income statement and a corresponding entry is made increasing accounts payable on the balance sheet. Paying the expense decreases cash and accounts payable (a liability is the opposite of an asset) on the balance sheet.

Sales are entered in the income statement as they occur and a corresponding entry is made increasing accounts receivable on the balance sheet. Getting paid for a service or sale increases cash and decreases receivables (both assets) on the balance sheet.

Balancing the Balance Sheet

The balance sheet accounts are measured at a moment in time, like a snapshot. They reflect a total of items at any particular time: a total of cash, accounts receivable, inventory, fixed assets, accounts payable, debts, investments and earnings retained in the company.

The income statement accounts are measured over a period of time, like a movie. They represent the sum total of transactions: sales, purchases, payroll, etc. The difference in sales less all related expenses equals the net income or loss for the period of time being measured.

BALANCE SHEET ACCURACY

It is easier to prove the accuracy of the balance sheet. Adding up how much each customer owes the store or reconciling cash to the bank statement is a much simpler process than attempting to add up each individual sales transaction on the income statement. For this reason, more time is actually spent on proving the accuracy of the balance sheet.

Once the balance sheet is proven, the income statement, in total, must be right! The only errors would be misclassifications, (i.e.: the phone bill could be incorrectly posted to the rent expense account).

The accounts of the income statement are generally reviewed for reasonableness by comparing amounts to prior periods and analyzing ratios. However, the accounts of the balance sheet are compared to actual totals of items counted (cash, receivables, inventory, payables, fixed assets, etc.).

Accounting Review Responsibilities

It is the responsibility of the CFO, controller or accounting manager to understand these concepts and to take the initiative to keep the financial statements as accurate as possible, regardless of how much an outside accounting service is utilized.

The CFO is responsible for creating and reviewing all period-end activities to ensure the period-end financial statements accurately reflect the results of the Company’s activities. The CFO should be familiar with the specific software procedures for keeping the prior year open until all final closing adjustments have been made and approved by the CFO.

Accounting is responsible for gathering all documentation required to complete the period-end closing and completing all ledger adjustments.

Closing the Open Period

“Closing” is the process of advancing from one month or period to the next or from one year to the next. In most computerized accounting systems the periods are closed by executing a menu command. The accounting month end close checklist usually involves nothing more than entering the next month and responding to the program’s suggestion to print various month-end reports. Even after moving to the next month, many accounting systems allow the user to return to previous months to enter or edit transactions.

The yearly closing is more rigorous since it involves re-setting all income statement accounts to zero. Once a year is “closed”, some accounting systems do not allow the user to go back or open a closed period to make changes. So be careful, once the period is closed, it is official and any adjustments that are required will need to be made in the current or next open period.

The financial statement is the most important management tool in financial accounting. An orderly, timely and comprehensive accounting review of all general ledger accounts will ensure an accurate representation of the company’s financial statements allowing for comparisons from one period to the next. Everyone in management should understand their financial statements and what they mean for the company.

Developing and accounting policy and procedure for Period-End Review & Closing helps to communicate the steps involved in review and closing, the responsibilities for each step, and should provide metrics for a timely closing process. Download a free sample accounting procedures to use as your own starting point to developing your own accounting policy manual.

Reviews

There are no reviews yet.