Streamline Your Inventory Counting Process with the Inventory Counting Procedure Template Word

Keeping track of inventory is crucial for any business, but it can be a time-consuming and tedious task. The Inventory Counting Procedure Template Word from Bizmanualz is designed to simplify the inventory counting process and ensure accuracy.

This template provides a step-by-step guide for conducting inventory counts, including instructions for preparing for the count, conducting the count, and reconciling any discrepancies. It also includes a customizable inventory count sheet to help you keep track of your inventory levels.

With the Inventory Counting Procedure Template Word, you can:

- Reduce the time and effort required for inventory counting

- Minimize errors and discrepancies in your inventory records

- Ensure compliance with industry regulations and standards

- Improve your overall inventory management processes

Whether you’re a small business owner or a large corporation, the Inventory Counting Procedure Template Word can help you streamline your inventory counting process and improve your bottom line. With easy-to-follow instructions and customizable templates, you can tailor the procedure to fit your specific needs and ensure that your inventory counts are accurate and efficient.

Don’t let inventory counting be a headache for your business. Invest in the Inventory Counting Procedure Template Word from Bizmanualz and take the first step towards a more streamlined and efficient inventory management process.

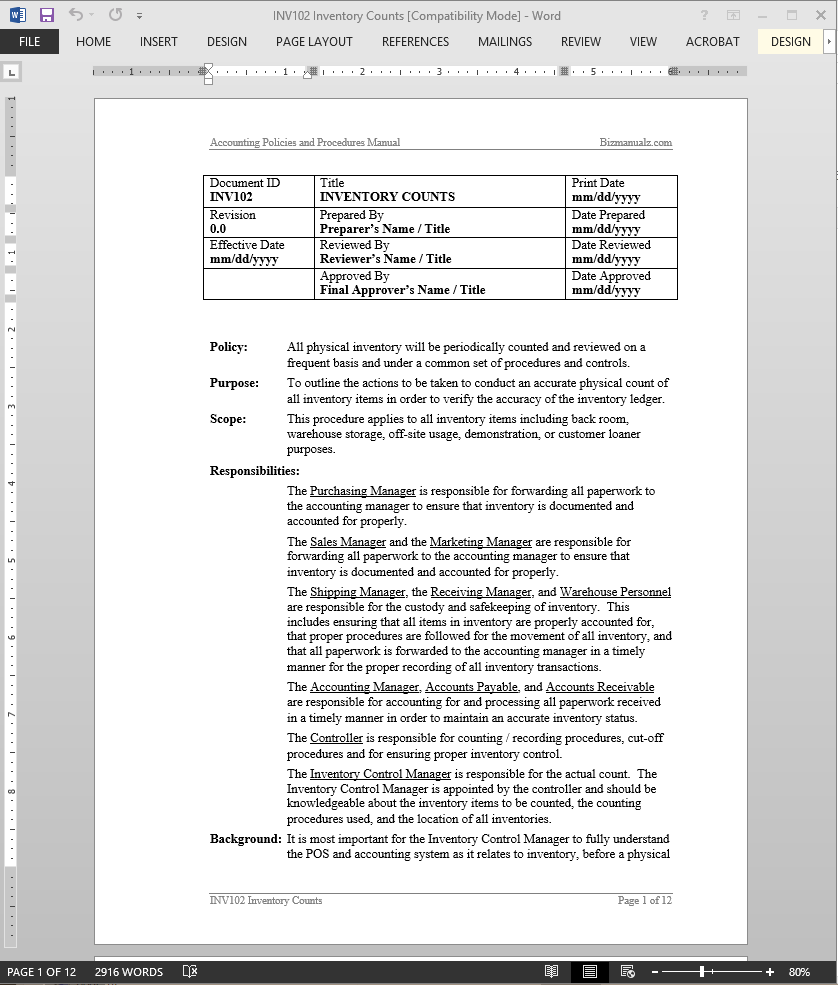

Inventory Counting Procedure

The Inventory Counting Procedure offers guidelines to ensure your physical inventory count and inventory ledger is consistent.

This Inventory Counting Procedure applies to all inventory stock from back room, warehouse storage, off-site usage, demonstration or customer loaner purposes. It should be utilized by the inventory control manager and purchasing, sales and marketing, accounting, accounts payable and receivable and warehouse personnel. (12 pages, 2866 words)

It is most important for the Inventory Control Manager to fully understand the POS and accounting system as it relates to inventory, before a physical inventory is taken. This includes an understanding of how the inventory is updated by customer returns, returns to vendors, transfers from inventory to internal use, adjustments for damaged or defective product, and backorders.

The inventory General Ledger balance is affected by every purchase and sale transaction that is processed through the REV102 POINT-OF-SALE (POS) procedure and the Accounting System. To maintain accuracy, one should periodically count the actual inventory on hand and then reconcile that count to the inventory General Ledger balance. Taking a complete physical count of all inventory items is one way to ensure that the balance is accurate.

Inventory Counting Responsibilities:

The Purchasing Manager is responsible for forwarding all paperwork to the accounting manager to ensure that inventory is documented and accounted for properly.

The Sales Manager and the Marketing Manager are responsible for forwarding all paperwork to the accounting manager to ensure that inventory is documented and accounted for properly.

Inventory Counting Procedure Activities

Inventory Counting Procedure Activities

- Inventory Types

- Preparation for Inventory Counting

- Period End Cut-off

- Complete Physical Count-Cost Method or “SKU” Method

- Complete Physical Count-Retail Method

- Cycle Count method

Reviews

There are no reviews yet.