Finance Policies Procedures Manual Template Word

The Finance Policies Procedures Manual Template Word is a comprehensive guide that provides a complete set of policies and procedures for managing financial operations in any organization. This manual is designed to help businesses establish a strong financial management system that is compliant with industry standards and regulations.

The manual includes customizable policies and procedures that cover all aspects of financial management, including treasury management, board of directors, financial reporting, and internal controls. The policies and procedures are written in clear and concise language, making them easy to understand and implement.

The Finance Policies Procedures Manual Template Word is ideal for businesses of all sizes, from small startups to large corporations. It is also suitable for non-profit organizations, government agencies, and educational institutions. The manual is fully customizable, allowing businesses to tailor it to their specific needs and requirements.

By using the Finance Policies Procedures Manual Template Word, businesses can ensure that their financial operations are efficient, effective, and compliant with industry standards and regulations. The manual provides a framework for managing financial operations that can be easily adapted to changing business needs and regulatory requirements.

In summary, the Finance Policies Procedures Manual Template Word is an essential tool for any business that wants to establish a strong financial management system. It provides a comprehensive set of policies and procedures that cover all aspects of financial management, making it easy for businesses to manage their finances effectively and efficiently.

Financial Policies Procedures Manual Template

Whether you are managing your financial processes, building financial internal controls or trying to improve your fiscal performance, Finance Policies Procedures Manual from Bizmanualz make the process much simpler and easier. This download only product comes in easily editable Microsoft Word templates to help you quickly and effectively implement strong financial internal controls.

Financial Policy Template Key Features

Introducing our comprehensive Finance Policies and Procedures Manual – the ultimate solution for businesses seeking to establish a robust financial framework. We understand the critical importance of maintaining sound financial management practices. That’s why we’ve meticulously designed this product to streamline your finance operations and ensure compliance with industry best practices and regulations.

A Complete Financial Handbook

Our Finance Policies and Procedures Manual covers every aspect of financial management, providing clear and concise guidelines on budgeting, accounting, reporting, and internal controls. Whether you’re a small startup or an established enterprise, this manual caters to businesses of all sizes and industries.

Customizable Financial Policy Templates

We recognize that every organization is unique, so we’ve included fully customizable templates that allow you to tailor policies and procedures to align with your specific needs and corporate culture. Say goodbye to one-size-fits-all solutions – our manual empowers you to create a finance framework that truly reflects your company’s objectives.

Stay Compliant and Audit-Ready

Compliance is non-negotiable when it comes to financial matters. Our Finance Policies and Procedures Manual helps you stay on top of regulatory requirements, enabling you to confidently navigate audits and inspections. Say goodbye to compliance headaches and hello to peace of mind. Implement a financial framework for board meetings, insider transactions, bank accounts, and other common financial practices.

Best Practices and Industry Standards

Our team of finance experts has distilled years of industry experience into this comprehensive manual. Benefit from proven best practices and stay updated with the latest financial management activities to keep your organization ahead of the competition.

Boost Financial Efficiency and Accountability

Efficient financial processes are the backbone of a successful company. With our financial policy guidelines, you’ll optimize financial workflows, reduce redundancies, and promote accountability across your finance team.

Empower Your Financial Team

Give your finance team the tools they need to excel. The Finance Policies and Procedures Manual fosters a culture of professionalism, standardization, and continuous improvement. Empower your employees to make better financial decisions that drive business growth.

Invest in your company’s financial future with our Finance Policies and Procedures Manual. Take the guesswork out of financial management and gain the confidence to make informed decisions that drive success. Visit [Link] today to see how our product can transform your finance department and elevate your business to new heights – Empowering Your Financial Success.

Instantly Develop Financial Policies that Answer Basic Financing Questions

The Bizmanualz Finance Policy Procedure Manual includes answers to basic financial questions:

- How do define your financial objectives?

- What’s your plan for business valuation or raising capital?

- What should be your policy on Related Party Transactions?

- What is the proper method for financial reporting?

- How do you hold a Board of Directors or Stockholders Meeting?

- How do you define, assess, or manage risk?

- What is the procedure for internal or external auditing?

These procedures cover key accounting and financial topics like capital planning, capital structure, asset and inventory control, financial reporting, and financial analysis. You will also get a free Small Business Management Guide that talks about planning, starting, managing and exiting a business.

“I have already recommended you to one of my colleagues who is looking for a policy and procedure manual.”

Bassam Hindy

Ernst & Young

Free Sample Financial Procedure

Download a free procedure from the finance manual right now with no obligation. You will get the entire table of contents and one actual policy and procedure set from the Finance Policy Procedure Manual.

Financial Best Practices Manual at Your Fingertips

It is not easy to write financial procedures from scratch. You can spend countless hours on research, writing, editing and review and yet fall short on all the requisite elements. The Financial Policy templates from Bizmanualz are thoroughly researched and are based on commonly recognized best practices. Why start from scratch when skilled finance professionals have already done the work for you?

The Financial Policies and Procedures Manual Template is organized into five categories:

Editable Financial Policies and Procedures in MS Word Templates

- Financial Administration

- Raising Capital

- Treasury Management

- Financial Statement Reporting

- Internal Controls

Fast Financial Internal Controls

The Finance Policies and Procedures Manual Template from Bizmanualz comes with 36 prewritten procedures, 61 forms, 10 job descriptions, a sample CFO’s manual, and a free Small Business Management Guide. Altogether, you get over 600 pages of content written by knowledgeable technical writers and reviewed by experienced CPA’s.

Financial Policies for Compliance and Control

Both the Securities and Exchange Commission (SEC) and the Public Company Accounting Oversight Board (PCAOB) clearly recognize policies and procedures as key elements of financial control. The Finance Policies and Procedures Manual is based on Generally Accepted Accounting Principles (GAAP) as well as standard best practices, and help you comply with regulatory requirements, standards, and guidelines for raising capital, treasury management (managing cash), financial statement reporting, financial auditing, and general financial administration.

Because of their generic and broad nature, the prewritten templates can be implemented by organizations of any size or kind.

What’s Included in the Finance Manual?

You will receive 614 pages of content within seven sections:

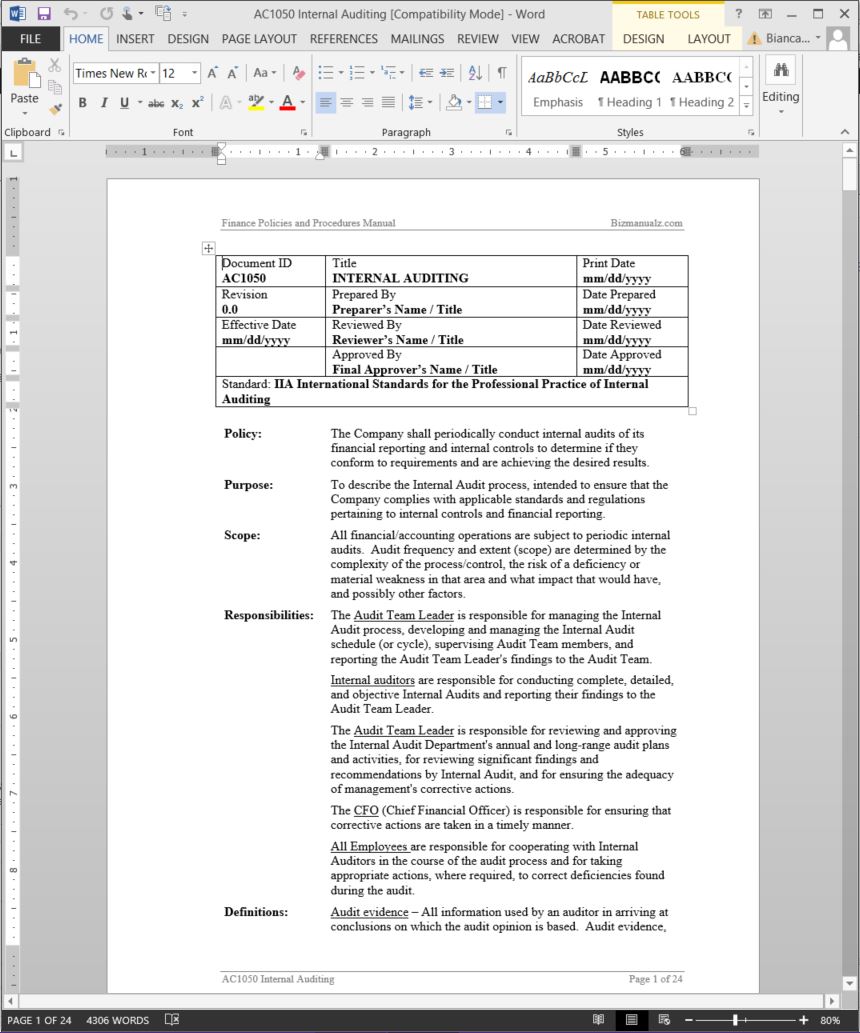

1. Finance Policy Manual Template

First, a 42 page Policy Manual is used as a top level document to all Finance policies governing your company’s Financial procedures.

2. Finance Manual Table of Contents

Next, 402 pages that include 36 prewritten Finance procedures, 57 Finance forms and corresponding activities–customize each Microsoft® Word document template to your needs.

3. Finance Job Descriptions

The Finance Manual also includes 34 pages with 10 Finance Job Descriptions covering the primary Finance Department.

4. Starting and Managing a Business

Free Bonus – Your Finance Manual also includes a guide to Starting and Managing a Business. Topics include business planning, financing, and basics to forming your business.

5. Introduction to Finance Training Guide

A 30 page training guide explains the basic concepts of Finance, its structure, standards and definitions, and more.

6. “How To” Manual Preparation Guide

A 42 page Procedure writing guide provides guidance to develop and implement your company’s Finance Policies and Procedures manual.

7. Finance Manual Keyword Index

Easily find what you are looking for inside the Finance Manual using the 18 page Keyword Index.

Free Sample Financial Procedure

Download a free procedure from the finance manual right now with no obligation. You will get the entire table of contents and one actual policy and procedure set from the manual. Or, if you are ready to buy now, place your order using our secure server and you’ll be able to download immediately. With our money-back guarantee, your purchase is risk-free!

Omer Osman Eltayeb (verified owner) –

downloading the graphs is a problem and carries your logo which makes it difficult for me to customize.

Hasan –

The Finance policies and procedures that we have bought are excellent, easy to understand and practical.

M.P. –

A very practical and user friendly guide to write and create new policies. Extremely helpful.

Patrick –

Policies, Procedures and Forms made my polices write up that much easier.

Cherrylet S –

I like the services that Bizmanualz do for their customer, how they can prompt response

to all the inquiry and question of their customer. Like for what I experience last time when

I purchase some books for our company. Once again, Thank you for the assistance of

Jan Fitzgerald.

Didi Mulyadi –

Excellent!

Acute Adeola Ibrahim –

I took a risk and bought the Finance manual on my own without approval from my boss who was away on summer vacation. There existed chances that I might not get the reimbursed. To my amazement, on his resumption, when I presented the the manual to him, he embraced it more than I thought. We ordered the. Accounting manual as well. Most importantly, I got my reimbursement!

Financial Controller –

I found it extremely helpful in drafting policies and procedures for my company.

Thomas Meyer –

I found the “Finance Policies, Procedures and Forms” manual to be the best generic finance policy & procedure manual on the market. It gave us the right wording to make our existing policies and procedures more effective and develop new policies and procedures where none existed. The references and additional resources have proven to be invaluable.